May Saw Soft Lumber Demand

Originally Published by: HBS Dealer — June 5, 2026

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

As forest industry folks returned to their desks following the respective Canadian and U.S. May long weekends, sentiment remained cautious.

The ongoing practice of hand-to-mouth business continued. Customers saw no reason to stock lumber inventory, placing orders for only the wood they knew they had immediate needs for.

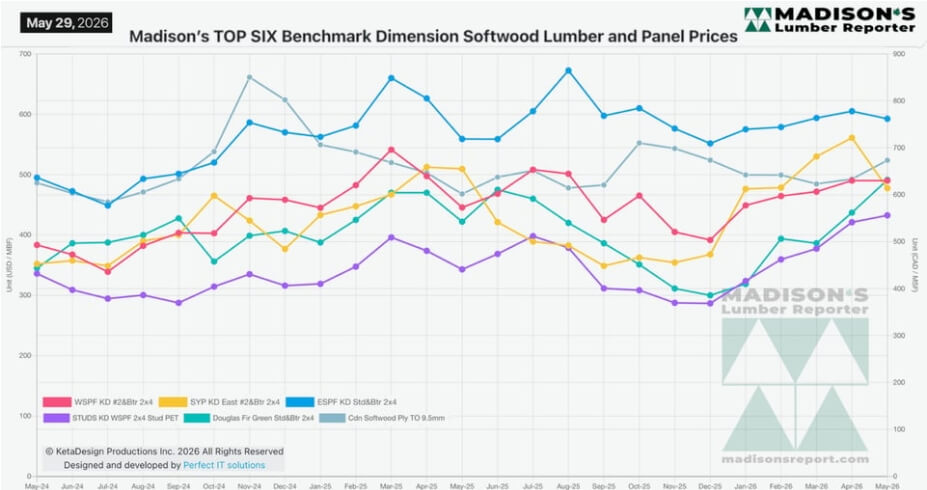

After a sizeable run-up earlier this year, Southern Yellow Pine East Side 2x4 price corrected all the way back down to where it had been in January and February. For its part, benchmark lumber item Western Spruce-Pine-Fir 2x4 prices steadily increased by nominal amounts, then stayed flat for two solid months.

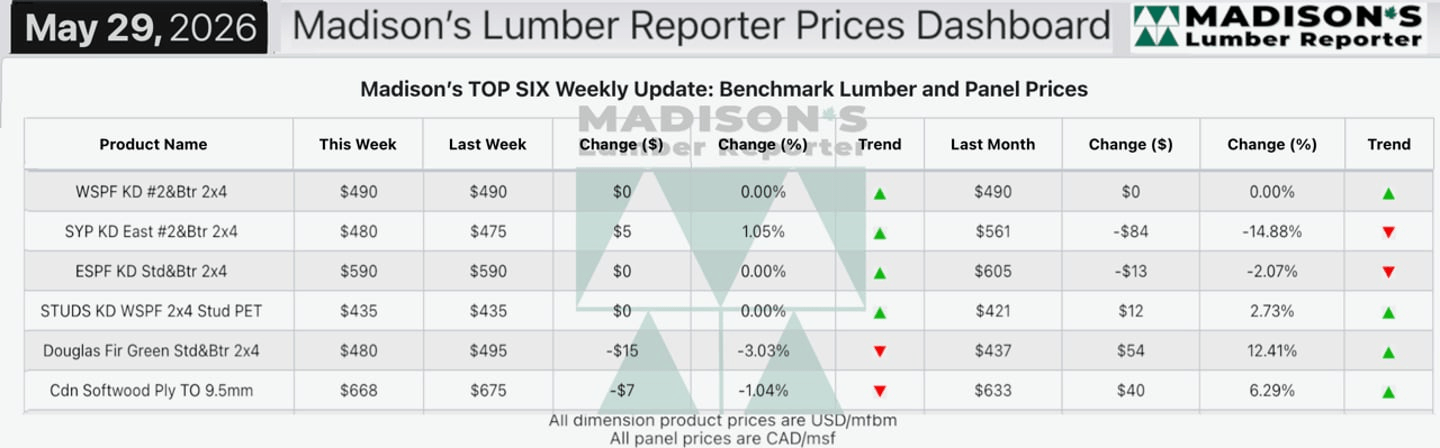

In the week ending May 29, 2026 the price of Western Spruce-Pine-Fir 2x4 #2&Btr KD (RL) was $490 mfbm, which was flat from the previous week, said weekly forest products industry price guide newsletter Madison's Lumber Reporter. That week's price was flat from one month ago when it was $490. Compared to the same week last year, when it was $450 mfbm, that price was up +$40, or +9%. Compared to two years ago when it was $384, that week's price was up +$106, or +28%.

In the week ending May 29, 2026, the price of Southern Yellow Pine East Side 2x4 #2&Btr KD (RL) was $480 mfbm. This was up +$5, or +1%, from the previous week when it was $475. That week's price was down -$81, or -14%, from one month ago when it was $561.

LUMBER PRICING AND MARKET CONDITIONS TAKEAWAYS, MAY 2026:

- Buyers of Western-SPF in the US remained focused on hand-to-mouth business on lacklustre downstream demand.

- Western-SPF sawmills in Canada held enough supply to satisfy current demand levels.

- There were a few pockets of challenging availability, with tighter supply in wider widths or straight lengths.

- Sawmill order files in the West were only into the first or second week of June.

- There was general apathy and lack of urgency among buyers of Eastern-SPF which is unusual for this time of year.

- Persistently high, and rising, costs of freight further reduced suppliers' margins.

- Southern Yellow Pine prices still settled on either side of the previous week's levels.

- Discounted SYP material thinned out dramatically as buyers had stepped in to shore up their depleted inventories.

- Eastern Stocking Wholesalers reported month-end machinations contributed to hesitation on the part of buyers.

The Madison's Lumber Prices Index for the week ending May 29, 2026 was: $521 mfbm. This was flat the previous week, and was down 0%, or -$1, from one month ago when it was $522.

Suppliers kept manufacturing volumes lower to stay in line with this soft demand. Along with the usual seasonal issues in transportation, specifically in sourcing trucks and rail cars, was sharply increasing fuel surcharges. Freight rates have ballooned significantly in the past couple of months, putting even greater pressure on costs for sawmills and other forest operators. In total, there was general apathy and lack of urgency among buyers which is unusual for this time of year.

Established in 1952, Madison's Lumber Prices is a premiere source for North American softwood lumber news, prices, industry insight and industry contacts. The weekly Madison's Lumber Reporter publishes current Canadian and U.S. construction framing dimension lumber and panel wholesaler pricing information 50 weeks a year and provides access to historical pricing as well.;

Kéta Kosman is editor, owner and publisher of Madison's Lumber Reporter. She covers breaking news for the softwood lumber market.