Lumber Prices Perk Up

Originally Published by: HBS Dealer — April 8, 2026

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

As March drew to a close, many lumber prices started to rise—albeit slightly.

Late-March levels were right in the middle, between those of the same time last year and in 2024. Despite an extended winter and soft demand, this is encouraging to the industry as regular seasonal price stability is best for planning.

Expectations for housing construction this year are for similar activity to last year, however no one really knows. At this time of great upheaval and much uncertainty, it is not clear how business will be as summer approaches.

For their part, sawmills had no plans to ramp up production volumes until there are obvious signs that improved demand will be ongoing. Customers, behaving with equal caution, continue to not stock inventory. If home building does increase this year, the very weak field inventories throughout the supply chain might become a problem for end-users.

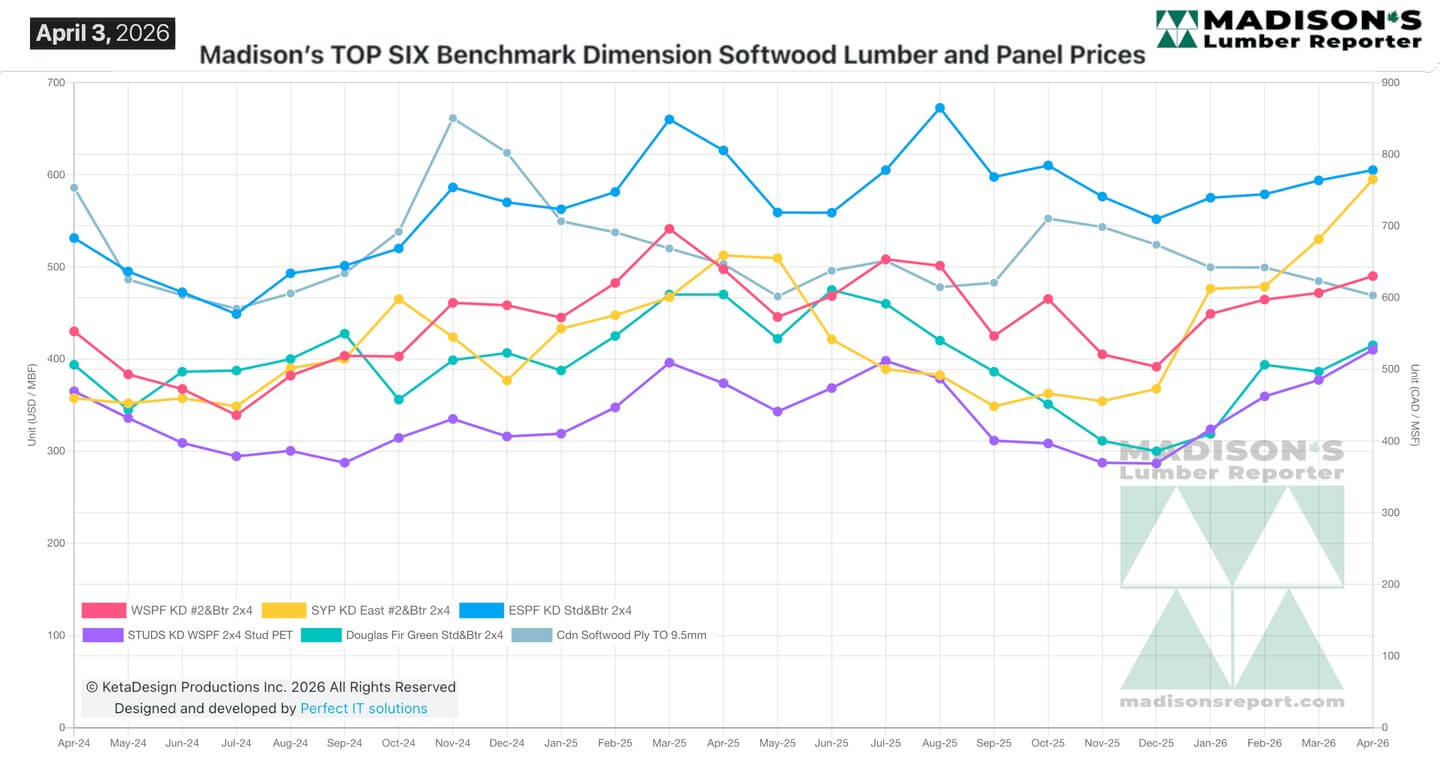

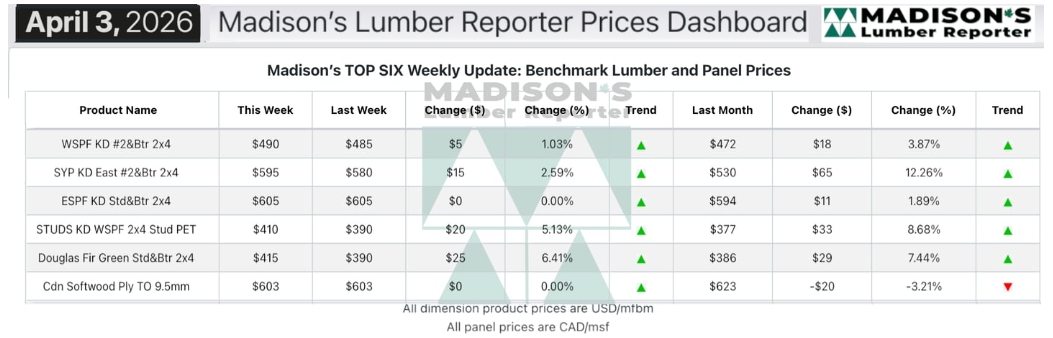

In the week ending April 3, 2026, the price of Western Spruce-Pine-Fir 2x4 #2&Btr KD (RL) was $490 mfbm, which was up +$5, or +1%, from the previous week when it was $485, according to weekly forest products industry price guide newsletter Madison’s Lumber Reporter. That week’s price was up +$18, or +4%, from one month ago when it was $472.

Compared to the same week last year, when it was $545 mfbm, that price was down -$55, or -10%. Compared to two years ago when it was $452, that week’s price was up +$28, or +6%.

Key lumber prices and market conditions takeaways from March 2026

- Sellers of Western-SPF in the US were inundated with orders and inquiry, such that they just had to focus on covering what demand they could.

- Improving spring weather fully activated construction in Texas, and started to percolate into the Central and Northern states.

- Limited mill availability continued to be exposed by even small jumps in demand as reduced supply among secondary suppliers surfaced.

- Buyers of Western-SPF in Canada stepped back to evaluate their positions heading into the Easter holiday long weekend break.

- Demand remained seasonally subpar as the calendar turned to April.

- Secondary suppliers showed adequate inventory levels and a willingness to negotiate.

- Canadians sawmills in the West maintained order files at around two- to three-weeks.

- All regions were affected by tightening truck supply and soaring freight rates.

- Customers of Eastern-SPF showed how underbought they were by calling back incessantly about where their latest order was in transit.

- Suppliers of Southern Yellow Pine tried to fulfill orders amid a rising market and severe ongoing freight challenges.

- In the U.S. Northeast, Douglas-fir suppliers boosted their asking prices as sawmills moved order files into late-April.

The Madison’s Lumber Prices Index for the week ending April 3, 2026 was: $522 mfbm. This was up +1%, or +$4, the previous week when it was $518 and was up +6%, or +$31, from one month ago when it was $491.

Established in 1952, Madison’s Lumber Prices is a premiere source for North American softwood lumber news, prices, industry insight and industry contacts. The weekly Madison’s Lumber Reporter publishes current Canadian and U.S. construction framing dimension lumber and panel wholesaler pricing information 50 weeks a year and provides access to historical pricing as well.