Chart: Residential Construction Loan Volume Grows

Originally Published by: NAHB — September 8, 2021

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

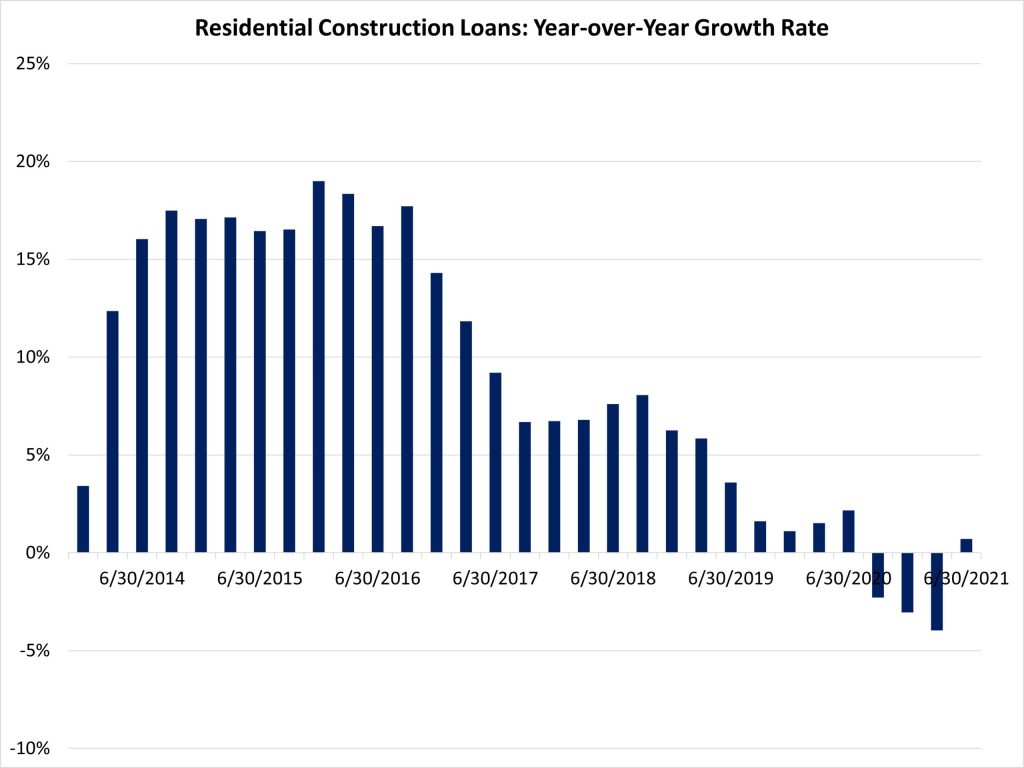

The second quarter of 2021 marked the second consecutive quarter of loan growth for residential construction loans. These gains have lifted the year-over-year growth rate, marking an expansion of outstanding loans for home builders.

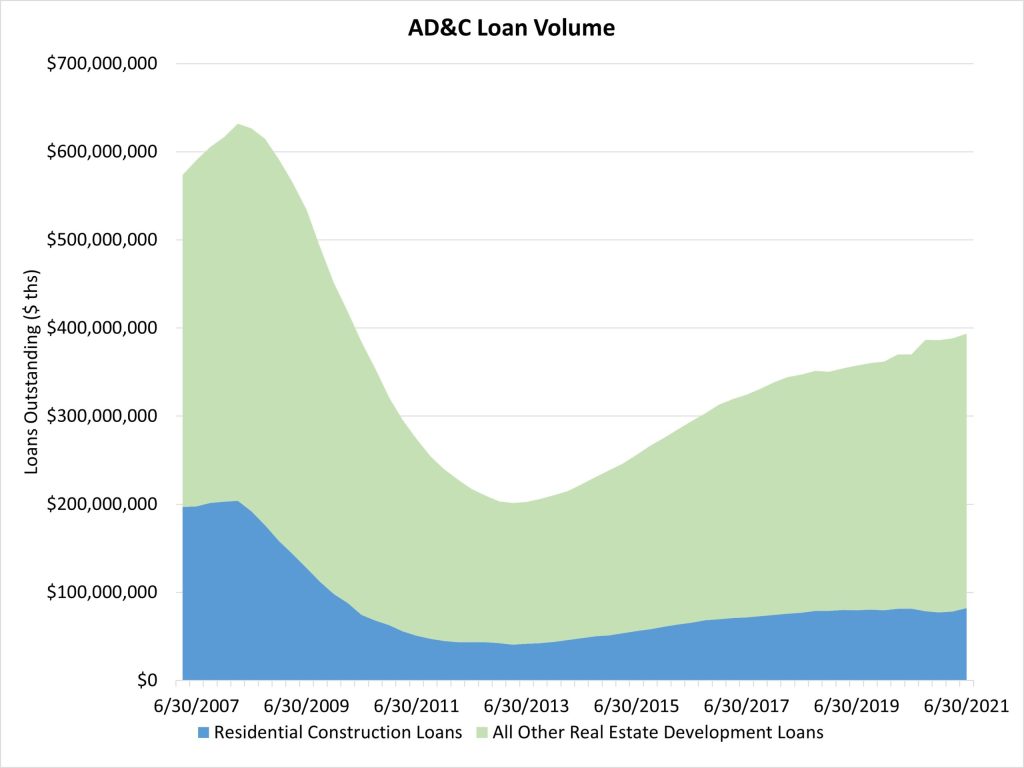

The volume of 1-4 unit residential construction loans made by FDIC-insured institutions increased by 4.9% during the second quarter, even as the market cooled off strong seasonally adjusted rates of construction from the second half of 2020. The volume of loans increased by $3.8 billion for the second quarter. This loan volume expansion placed the total stock of home building construction loans at $82 billion, a post-Great Recession high.

On a year-over-year basis, the stock of residential construction loans is up 0.7%. Since the first quarter of 2013, the stock of outstanding home building construction loans has grown by 101%, an increase of almost $41.3 billion.

- ADVERTISEMENT -

It is worth noting the FDIC data represent only the stock of loans, not changes in the underlying flows, so it is an imperfect data source. Lending remains much reduced from years past. The current amount of existing residential AD&C loans now stands 60% lower than the peak level of residential construction lending of $204 billion reached during the first quarter of 2008. Alternative sources of financing, including equity partners, have supplemented this capital market in recent years.

The FDIC data reveal that the total decline from peak lending for home building construction loans continues to exceed that of other AD&C loans (nonresidential, land development, and multifamily). Such forms of AD&C lending are off a smaller 28% from peak lending. For the second quarter, these loans posted a 0.4% increase, a possible indication of increased land development activity.