Latest Home Builders Sales Survey Results Indicate Persistent Headwinds

Originally Published by: HBS Dealer — June 22, 2026

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

The latest monthly BTIG/HomeSphere Homebuilder Survey, which solicits the perspective of small- and mid-sized tract and custom homebuilders nationally about sales, customer traffic, and pricing trends, came in relatively flat month-over-month after two months of weakening results.

Twenty-eight percent of builders saw higher year-over-year sales in May, improving

from 24% in April, and 27% saw lower sales vs. 32% in April.

Traffic trends were more mixed, as only 20% of builders reported higher year-over-year traffic, the lowest level since November 2023. The traffic results, per BTIG, suggest the

cumulative effect of higher rates (and inflation more generally) seen since February could

be pushing potential buyers to the sidelines.

Sales and traffic relative to expectations were also relatively flat from April. Pricing and incentives weakened somewhat as more builders reported lower prices and higher incentives than in April. Builder commentary remained subdued in May, with most pointing to a slow spring selling season.

The big takeaway from BTIG: Higher rates, higher prices and weaker consumer sentiment appeared to continue to impact demand in May, requiring higher incentives and lower prices to drive sales. The incentive and price activity appears to have supported sales despite lower traffic, likely at the expense of profits given mostly flat sales vs. expectations.

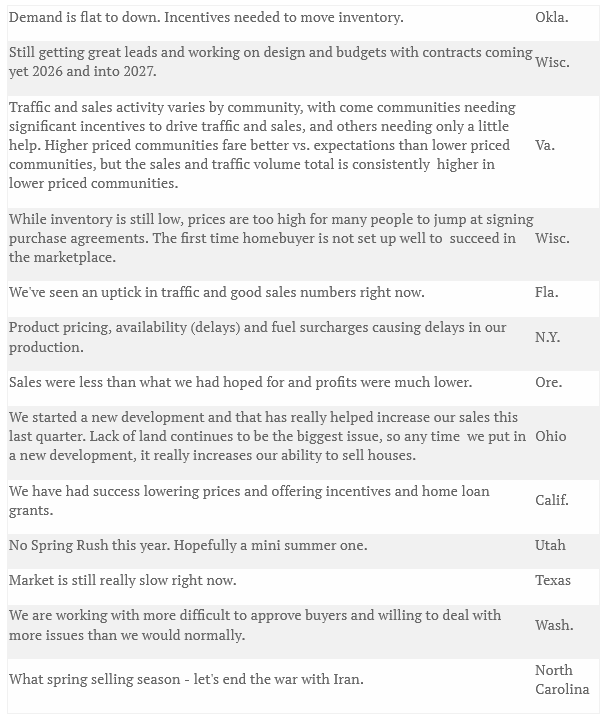

Get more data below, along with comments shared by builders in specific states.

Sales & traffic. Sales looked moderately better in May after March and April

declines. Twenty-eight percent of respondents reported higher y/y sales in May vs. 24% in April, and 27% of respondents reported lower y/y sales vs. 32% in April.

Traffic trends were mixed. A quarter of respondents reported lower y/y traffic, an improvement from 29% in April, but 20% reported higher traffic, down from 29% in April and a recent high of 43% in February.

Sales & traffic relative to expectations. Sales and traffic relative to expectations

were relatively flat in May. Thirty percent of respondents saw sales as better than expected (27% in April), and 37% saw sales as worse (35% in April).

Twenty-eight percent of builders saw better-than-expected traffic, flat from April, and 24% saw it as worse vs. 26% in April.

Base pricing. The percentage of builders raising some, most or all base prices

declined to 17% from 20% in April. The percentage of builders lowering some, most,

or all base prices increased to 27% vs. 24% in April.

Incentives. Twenty-nine percent of survey respondents reported increasing some, most, or all incentives in May, up from 28% in April. Only 3% reported decreasing incentives, and 56% left incentives unchanged.

Builder commentary. Most builders highlighted a weak selling season affected by

high prices and interest rates. Some builders noted higher incentives successfully

spurred sales activity. A few builders pointed to an uptick in demand. Below are some specific comments shared by builders around the U.S.