New Home Sales Rise 7.5% in October

Originally Published by: NAHB — December 2, 2022

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

NAHB Chief Economist Robert Dietz recently provided the following housing industry overview in the bi-weekly e-newsletter Eye on the Economy.

Mortgage interest rates have stabilized in recent weeks, as the bond market deals with the expectation of tighter monetary policy from the Federal Reserve. Although the Fed’s actions will likely continue to place upward pressure on rates into 2023, the rising possibility of a broader macroeconomic slowdown would ultimately lead rates to level off and eventually decline. Per Freddie Mac, the average 30-year fixed-rate mortgage for the week of Nov. 23 stood at 6.58%, the lowest since the second half of 2022.

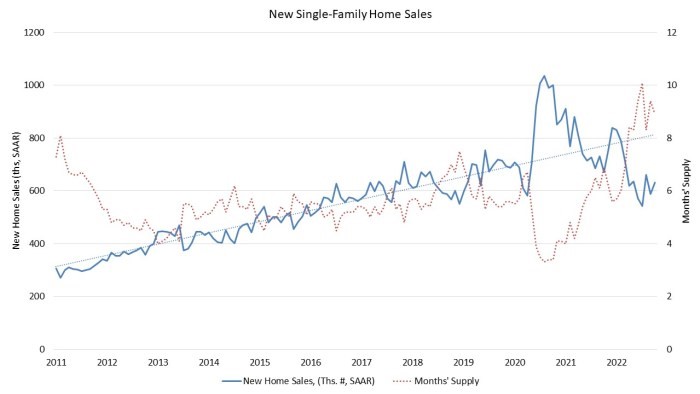

As a result, October sales of newly built, single-family homes registered at a 632,000 seasonally adjusted annual pace, which is a 7.5% monthly increase and is 5.8% below the October 2021 estimate of 671,000 per Census data. However, the Census data do not include cancelled sales, which are likely running at a 25% rate (compared to 9% a year ago). Regardless, the pace of sales has slowed significantly, as evidenced by the fact that completed, ready-to-occupy inventory is rising while the inventory of homes not started is falling in response to weaker demand.

This long-run trend for housing demand is reflected in the data for existing home sales, which fell 5.9% in October to a seasonally adjusted annual rate of 4.43 million per the National Association of Realtors. This was the lowest pace since December 2011, with the exception of April and May 2020. On a year-over-year basis, sales were down 28.4%.

The pullback in housing demand is now causing home prices to fall. The S&P CoreLogic Case-Shiller national home price index fell at a seasonally adjusted annual growth rate of 8.7% in September, the third consecutive monthly decline. Nonetheless, national home prices are now 62.4% higher than their last peak during the housing boom in March 2006. Prices will continue to decline going into 2023 because of lower traffic numbers.

However, there are some submarkets showing ongoing, positive conditions. For example, custom home building expanded during the third quarter of 2022, with 59,000 total starts. This marks a 5% increase compared to the third quarter of 2021. Over the last four quarters, custom housing starts totaled 207,000 units, a 9% gain from the prior four-quarter total. Custom construction likely benefited from improved supply chains, a reduction in the growth rate of the cost of building materials and a stock market rally that helped the higher end of the market.

The broader housing contraction is now spreading to the rental market, at least according to leading indicators. Confidence in the market for new multifamily housing declined significantly in the third quarter of 2022. The NAHB Multifamily Production Index (MPI) decreased 10 points to 32 compared to the previous quarter. The MPI is a leading indicator of future trends within the apartment construction market, which as of the third quarter, is 97% built-for-rent. Multifamily development is likely to fall back in 2023 due to a large amount of supply in the construction pipeline that will slow rent growth, as well as the expectation of rising unemployment in the coming quarters.